With an aging population and a changing work landscape, pensions are more important than ever. But for many in the UK, navigating the world of pension providers can feel overwhelming. This article aims to be your guide, unpacking the key factors to consider when choosing the best pension provider for your needs.

Understanding Your Options: Workplace Pensions vs. Personal Pensions

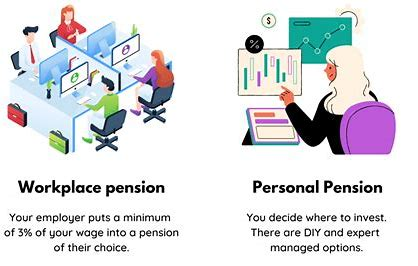

The first step is understanding the pension landscape. Most UK employees will be automatically enrolled in a workplace pension.

Employers contribute alongside your salary deductions, offering a valuable head start on retirement savings. However, you might also consider a personal pension (SIPP) for additional flexibility and investment control.

Workplace Pensions: The Basics

NEST vs. Private Providers:

Most employers choose a private pension provider for their workplace pension scheme. However, some may utilize NEST, a government-backed provider offering a low-cost option.

Your Choice is Limited:

The provider for your workplace pension is typically pre-selected by your employer. While you can’t change the provider, you may have some control over the investment options within the scheme.

Personal Pensions (SIPPs): Freedom and Flexibility

Greater Investment Choice:

With a SIPP, you have a wider range of investment options compared to a typical workplace pension. This allows you to tailor your investments to your risk tolerance and retirement goals.

Transferring Existing Pensions:

SIPPs allow you to consolidate existing pensions from previous employers, simplifying your retirement planning.

Increased Fees:

SIPPs typically come with higher fees compared to workplace pensions. These fees can include platform charges, fund charges, and dealing fees.

Choosing the Right Provider: Key Considerations

Once you’ve determined whether a workplace pension or SIPP is right for you, it’s time to evaluate potential providers. Here are the key factors to consider:

Fees and Charges:

Compare annual fees, fund charges, and transaction fees across different providers. Lower fees can significantly impact your retirement pot over time.

Investment Performance:

Research the past performance of the investment funds offered by different providers. Remember, past performance doesn’t guarantee future results.

Customer Service:

Having access to helpful and responsive customer service is crucial for managing your pension effectively. Check online reviews and consider contacting providers directly to gauge their service quality.

Online Tools and Resources:

A user-friendly online platform allows you to easily monitor your pension performance, make contributions, and adjust your investment strategy.

Company Reputation:

Research the provider’s track record and financial stability. Look for providers with a strong reputation for transparency and ethical practices.

Beyond the Basics: Additional Factors to Consider

Automatic Investment:

Look for providers with features that automate contributions, ensuring you stay on track with your retirement savings goals.

Ethical Investment Options:

If ethical considerations are important to you, choose a provider offering investment funds that align with your values.

Socially Responsible Investing (SRI):

Some providers offer SRI options that focus on companies committed to environmental and social responsibility.

Popular Pension Providers in the UK: A Starting Point

Here’s a list of some of the leading pension providers in the UK, though this is not an exhaustive list and it’s important to conduct your own research:

Remember, the “best” provider depends on your individual needs and circumstances. Carefully evaluate the factors mentioned above to identify the provider that best aligns with your long-term retirement goals and financial comfort level.

Final Thoughts: Taking Charge of Your Future

Choosing a pension provider is a crucial decision. By educating yourself and carefully considering the options available, you can empower yourself to secure a comfortable and financially secure retirement.

Don’t hesitate to seek professional financial advice if needed, especially when navigating the complexities of SIPPs and investment strategies. Remember, a well-chosen pension provider can significantly impact your financial well-being in your golden years.

FAQs

Q: Are there government incentives for saving into a pension?

Yes! The UK government offers tax relief on pension contributions, essentially giving you a tax break for saving for retirement.

Q: What if I’m self-employed? Can I still get a pension?

Absolutely! You can set up a personal pension or a stakeholder pension, a type of personal pension designed specifically for the self-employed.

Q: How much do pension provider fees typically cost?

Fees can vary, so comparing them is crucial. Annual management charges typically range from 0.5% to 1.5% of your pension pot.

Q: What investment options do pension providers typically offer?

Providers offer a range of funds, from low-risk options like bonds to higher-risk but potentially higher-reward options like stocks.

Q: How do I choose the right investment mix for my pension?

Consider your age, risk tolerance, and retirement goals. Younger individuals can typically handle higher risk for potentially greater returns.

Q: Where can I find information about a pension provider’s investment performance?

Many providers publish their investment performance records on their websites. Independent financial websites can also offer insights.

Q: How important is customer service when choosing a pension provider?

Having easy access to helpful customer service is essential for managing your pension and resolving any issues.

Q: What should I look for in terms of customer service?

Look for providers with clear online resources, readily available phone support, and a transparent complaint handling process.

Q: Can I transfer my existing pension to a new provider?

Yes, transferring your pension is usually possible, but check with your current provider about any exit fees.

Q: What are the benefits of transferring my pension?

You might find a provider with lower fees, a wider investment choice, or better customer service.

Q: What if I’m unsure about choosing a pension provider?

Seeking professional financial advice can be beneficial, especially if your financial situation is complex.

Q: How can I compare different pension providers uk ?

Many financial comparison websites allow you to compare fees, investment options, and customer reviews of different providers.

Q: Is a big-name provider automatically the best option?

Not necessarily. Bigger providers aren’t always cheaper, and smaller providers might offer competitive rates and personalized service.

Q: Should I choose a provider with the highest investment returns?

Past performance doesn’t guarantee future results. Choose a provider with a solid track record and investment options that suit your risk tolerance.

Q: How much should I be saving into my pension?

There’s no one-size-fits-all answer, but aiming for 10-15% of your salary is a good starting point.

To read more click here